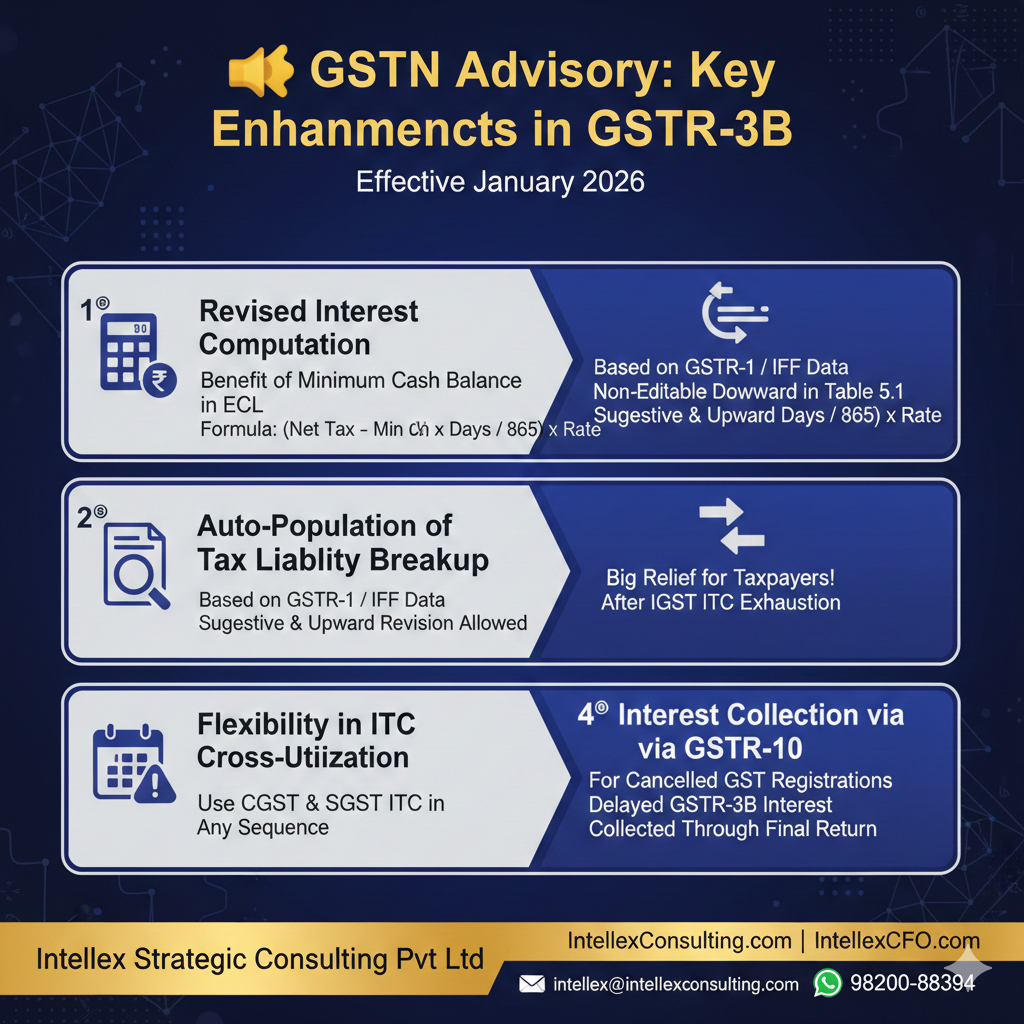

GSTN Advisory: Key Enhancements in GSTR-3B Reporting (Effective January 2026)

Stay compliant with the latest January 2026 GSTN enhancements.

Explore detailed insights into revised interest computation under Rule 88B, automated liability breakup in GSTR-3B, and flexible ITC utilization strategies.

Effective from the January 2026 tax period, the Goods and Services Tax Network (GSTN) has implemented significant systemic updates to Form GSTR-3B. These enhancements aim to automate interest calculations, streamline Input Tax Credit (ITC) utilization, and ensure stricter adherence to Rule 88B of the CGST Rules, 2017.

1. Revised Interest Computation (Table 5.1)

In compliance with Rule 88B(1), the system now automates interest calculations by accounting for the liquidity available in a taxpayer’s Electronic Cash Ledger (ECL).

- The “Cash Balance” Benefit: Interest is now calculated on the net tax liability after deducting the minimum cash balance maintained in the ECL from the return due date until the actual date of discharge.

- System Constraints: The auto-populated interest in Table 5.1 is non-editable downwards. While taxpayers cannot reduce the system-computed amount, they are permitted (and encouraged) to make upward adjustments if their self-assessed liability is higher.

- Implementation: These changes apply to delayed filings for Jan-2026 onwards, with the computed interest appearing in the Feb-2026 return.

2. Automation of Tax Liability Breakup

To enhance transparency, the Tax Liability Breakup Table—accessible via Table 6.1 (Payment of Tax)—is now auto-populated by the portal.

- Data Sourcing: The system aggregates data based on invoice dates and supplies reported in GSTR-1, GSTR-1A, or the Invoice Furnishing Facility (IFF).

- Functionality: This table distinguishes between current period liabilities and adjustments for previous periods. While the values are suggestive, taxpayers may revise them upwards to ensure full disclosure.

3. Enhanced Flexibility in ITC Cross-Utilization

The January 2026 update introduces a significant ease-of-business measure regarding the utilization of credits in Table 6.1.

- The Rule: Once the Integrated GST (IGST) credit is fully exhausted, the portal now allows taxpayers the flexibility to discharge IGST liabilities using CGST and SGST credits in any preferred sequence.

- Impact: This removes rigid systemic hurdles and allows for more efficient management of credit balances across different heads.

4. Interest Collection via GSTR-10 (Final Return)

For taxpayers with cancelled registrations, the GSTN has integrated an enforcement mechanism within the Final Return.

- Mechanism: If the final GSTR-3B was filed after the statutory due date, any applicable interest on that delay will now be automatically levied and collected through Form GSTR-10.

Strategic Support and Compliance Excellence

Navigating the complexities of evolving GST regulations requires proactive financial oversight and technical expertise. Intellex Strategic Consulting Pvt Ltd provides specialized end-to-end solutions to ensure your business remains compliant while optimizing its tax positions. Whether you require comprehensive guidance in Statutory Compliances or the sophisticated financial leadership of a Virtual CFO, our team is equipped to drive your operational excellence.

To learn more about our services, visit us at IntellexConsulting.com or IntellexCFO.com. For expert consultation, contact us via email at intellex@intellexconsulting.com or via WhatsApp at 98200-88394.

Team: Intellex Strategic Consulting Pvt Ltd

More Featured Articles:

Finance Bill 2026 to Revolutionize GST with Faster Registration and 90% Automatic Refunds

Secured and Un-Secured Financial Products from Bajaj Finance Ltd

Startup India Registration: Unlocking Tax Benefits and Growth

Why MSMEs Trust Us With Their Most Critical Financial Decisions

Funding & Investment Options to Grow India’s Real Estate & Allied Businesses

SME IPO in India 2025: Complete Guide for Investors & Growing Businesses

Loans Takeover proposals with enhancement of Banking limits for MSME Sector Companies

Tax implications on Diwali Gifts, Perquisites & any kind of Gifts in India