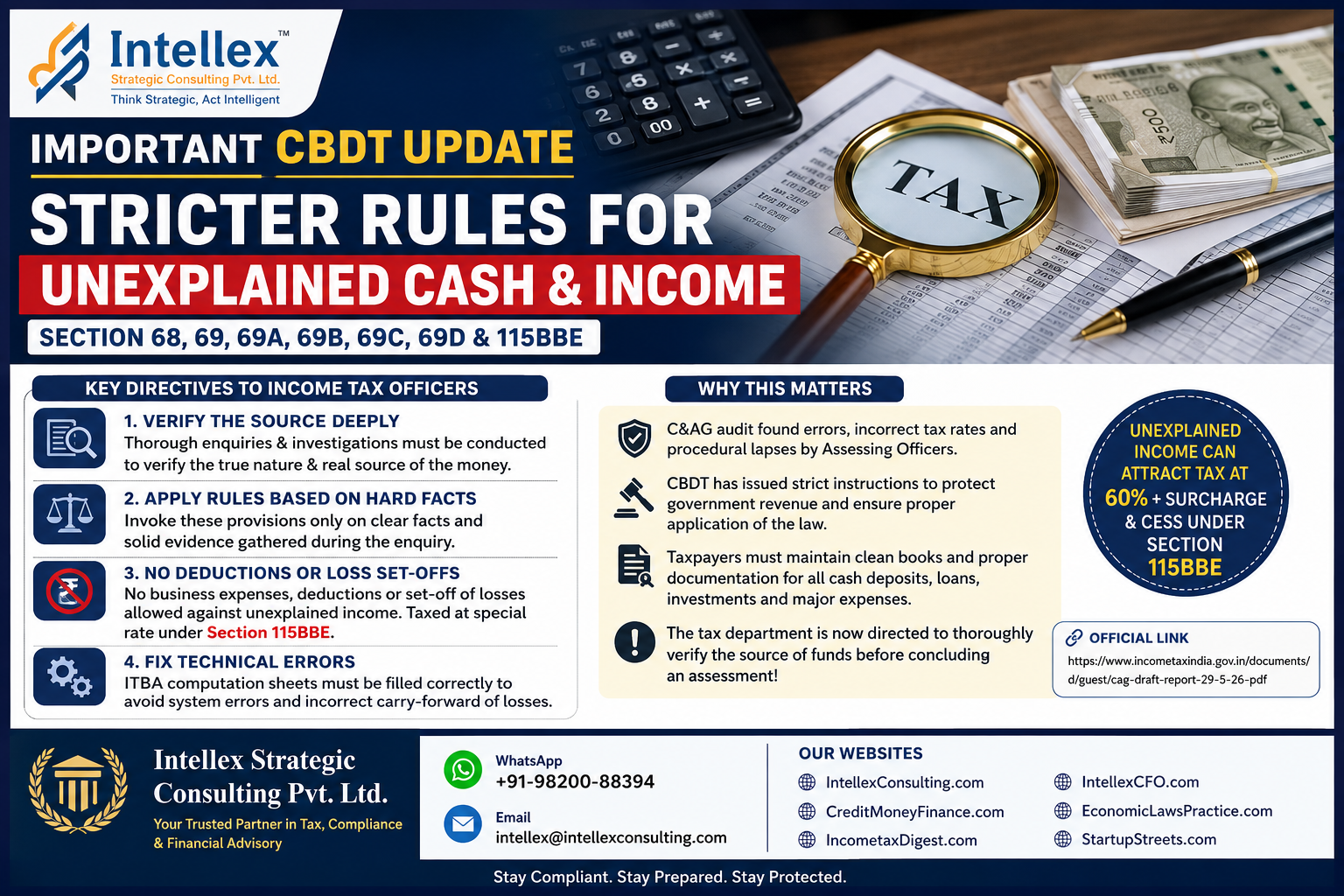

CBDT Issues Strict Instructions on Unexplained Cash & Income: Major Compliance Changes Under Sections 68, 69 & 115BBE for Taxpayers in 2026.

The CBDT has issued strict directions to Income Tax Officers regarding unexplained cash credits, investments, expenses, and income under Sections 68, 69, 69A, 69B, 69C, 69D and Section 115BBE. Learn the latest compliance requirements, tax implications, penalties, and documentation standards for taxpayers.

CBDT Tightens Enforcement on Unexplained Cash, Investments and Income: What Taxpayers Must Know About Sections 68, 69 and 115BBE

In a significant move aimed at strengthening tax administration and preventing revenue leakage, the Central Board of Direct Taxes (CBDT) has issued fresh instructions to Income Tax Department field officers following observations made by the Comptroller and Auditor General of India (C&AG).

The latest directive addresses serious deficiencies noticed during tax assessments involving unexplained cash credits, investments, expenditures, and other unexplained income covered under Sections 68, 69, 69A, 69B, 69C, and 69D of the Income-tax Act, 1961.

The CBDT has directed all Assessing Officers (AOs) across the country to exercise greater diligence, conduct proper investigations, and ensure the correct application of tax provisions, particularly the stringent provisions of Section 115BBE.

The move is expected to increase scrutiny of cash transactions, unsecured loans, share capital, investments, high-value expenditures, and other transactions where taxpayers are unable to satisfactorily explain the source of funds.

Background: Why Did CBDT Issue These Instructions?

The trigger for the new instructions was a compliance audit conducted by the Comptroller and Auditor General of India (C&AG).

The audit identified several instances where Assessing Officers:

- Failed to properly verify the source of funds.

- Applied incorrect tax rates.

- Did not invoke the appropriate statutory provisions.

- Allowed deductions or set-offs that were legally not permissible.

- Made computational mistakes in assessment orders.

- Incorrectly carried forward losses despite additions under unexplained income provisions.

These errors resulted in potential loss of tax revenue and inconsistent application of tax laws.

To address these concerns, CBDT has now directed all field formations to strictly follow the law while making assessments involving unexplained income.

Understanding the Relevant Sections

Section 68 – Unexplained Cash Credits

Section 68 applies when any sum is found credited in the books of a taxpayer and the taxpayer cannot satisfactorily explain:

- Identity of the creditor,

- Creditworthiness of the creditor, and

- Genuineness of the transaction.

Common examples include:

- Unsecured loans

- Share capital received by companies

- Share premium receipts

- Cash deposits

- Advances from unknown parties

If the explanation is unsatisfactory, the amount may be treated as taxable income.

Section 69 – Unexplained Investments

This section applies when investments are discovered but are not recorded in the books of accounts and the taxpayer fails to explain the source.

Examples include:

- Purchase of land

- Property investments

- Gold and jewellery purchases

- Financial investments not disclosed in books

Section 69A – Unexplained Money, Bullion, Jewellery or Valuable Articles

This section covers cases where:

- Cash is found during searches or surveys.

- Jewellery is discovered.

- Valuable assets are identified.

- The taxpayer cannot satisfactorily explain ownership or source.

Section 69B – Investments Not Fully Disclosed

This provision applies when the Income Tax Department finds that:

- Actual investment exceeds the amount disclosed.

- The taxpayer has understated the purchase value of an asset.

For example, a property purchased for ₹1 crore may have been recorded at only ₹70 lakh.

Section 69C – Unexplained Expenditure

Where a taxpayer incurs expenditure but cannot explain the source of funds used, the amount may be deemed income.

Examples include:

- Luxury weddings

- Foreign travel

- High-value personal spending

- Business expenditures without funding evidence

Section 69D – Certain Borrowings and Repayments

This section deals with borrowings and repayments made through non-compliant instruments or undocumented arrangements.

Section 115BBE: The Harsh Tax Provision

One of the most important aspects highlighted by CBDT is the mandatory application of Section 115BBE.

This provision imposes a special tax regime on unexplained income assessed under Sections 68 to 69D.

The income is taxed at:

- 60% basic tax

- 25% surcharge on tax

- 4% health and education cess

The effective tax burden can exceed 78% including applicable penalties in certain situations.

The intention behind this provision is to discourage concealment of income and the introduction of unaccounted money into the financial system.

Key CBDT Instructions to Assessing Officers

1. Thorough Verification of Source of Funds

CBDT has directed officers not to make additions mechanically.

Before invoking Sections 68 to 69D, officers must:

- Conduct proper enquiries.

- Examine supporting evidence.

- Verify the true source of funds.

- Establish facts through investigation.

The emphasis is on evidence-based assessment rather than presumptive additions.

2. Reliance on Facts and Documentary Evidence

Assessing Officers have been instructed that additions should be supported by:

- Documentary records

- Bank statements

- Financial trails

- Independent verification

- Investigation findings

This instruction seeks to reduce arbitrary assessments and improve legal sustainability of tax orders.

3. No Deductions or Loss Set-Off Against Unexplained Income

CBDT has once again clarified that income assessed under Sections 68 to 69D:

Cannot be reduced by:

- Business losses

- Capital losses

- Unabsorbed depreciation

- Chapter VI-A deductions

- Other expenditure claims

Taxpayers often attempt to offset such additions against carried-forward losses. CBDT has reiterated that such adjustments are not permissible under Section 115BBE.

4. Correct Use of ITBA Computation System

The Income Tax Business Application (ITBA) portal is used for assessment and computation of tax liabilities.

CBDT has directed officers to:

- Fill all computation fields correctly.

- Record additions under the correct section.

- Avoid incorrect carry-forward of losses.

- Prevent system-generated errors.

Proper digital reporting is now a key compliance requirement for tax authorities themselves.

Practical Impact on Taxpayers

The new instructions signal a stricter compliance environment.

Taxpayers should expect increased scrutiny of:

Cash Deposits

Particularly where:

- Large amounts are deposited in bank accounts.

- Source documentation is weak.

- Transactions are inconsistent with declared income.

Unsecured Loans

Tax authorities will closely examine:

- Identity of lenders.

- Bank trails.

- Financial capacity of lenders.

Share Capital and Share Premium

Private companies receiving investments may face enhanced verification requirements.

Property Transactions

Real estate purchases and investments may be compared with market intelligence and third-party information.

High-Value Expenditure

Luxury spending, foreign travel, events, and asset acquisitions may require stronger source documentation.

How Taxpayers Can Protect Themselves

To avoid additions under Sections 68 and 69, taxpayers should maintain:

Proper Banking Records

Ensure all transactions are traceable through banking channels.

Loan Documentation

Maintain:

- Loan agreements

- PAN details

- Bank statements

- Income proofs of lenders

Investment Records

Keep:

- Purchase deeds

- Payment records

- Source of funds documentation

Expense Evidence

Maintain invoices, bills, contracts, and payment proofs for major expenditures.

Reconciliation Statements

Regularly reconcile:

- Books of accounts

- Bank balances

- Investments

- Financial statements

Increased Litigation Likely

Tax professionals expect these instructions to result in:

- Increased scrutiny assessments.

- More notices seeking explanations.

- Greater use of information collected through AIS and data analytics.

- Enhanced verification of financial transactions.

- Higher tax demands where documentation is inadequate.

However, the CBDT’s emphasis on evidence-based assessments may also help reduce arbitrary additions and improve fairness in tax administration.

Expert Analysis

The CBDT’s latest instruction represents a dual message:

For Tax Officers

- Follow the law carefully.

- Conduct proper investigations.

- Apply the correct tax provisions.

- Avoid procedural and computational errors.

For Taxpayers

- Maintain complete documentation.

- Ensure transparency in financial transactions.

- Be prepared to explain the source of funds.

- Strengthen compliance systems and record keeping.

As data analytics, AIS reporting, GST integration, banking information, and digital financial trails become more sophisticated, unexplained cash and undocumented transactions are increasingly likely to attract departmental attention.

Conclusion

The CBDT’s latest directive marks a significant tightening of enforcement relating to unexplained income under Sections 68, 69, 69A, 69B, 69C and 69D of the Income-tax Act.

Taxpayers must recognize that unexplained cash deposits, investments, loans, and expenditures can now face deeper scrutiny and attract taxation under the stringent provisions of Section 115BBE, where deductions and loss set-offs are not available.

Maintaining robust documentation, transparent banking trails, and accurate accounting records is no longer merely a best practice—it has become an essential compliance requirement in today’s data-driven tax environment.

Official Reference

CBDT Instruction based on C&AG Audit Report:

https://www.incometaxindia.gov.in/documents/d/guest/cag-draft-report-29-5-26-pdf

Professional Assistance

Intellex Strategic Consulting Pvt. Ltd.

For assistance relating to:

- Income Tax Assessments

- Scrutiny Notices

- Section 68 & 69 Matters

- Tax Litigation & Appeals

- Tax Compliance Reviews

- CFO & Advisory Services

- Corporate Tax Planning

- Financial Documentation & Risk Management

WhatsApp: +91-98200-88394

Email: intellex@intellexconsulting.com

Websites:

- IntellexConsulting.com

- CreditMoneyFinance.com

- IncometaxDigest.com

- IntellexCFO.com

- EconomicLawsPractice.com

- StartupStreets.com

Intellex Strategic Consulting Pvt. Ltd. provides comprehensive tax, regulatory, financial, compliance, and advisory solutions to businesses, startups, professionals, and high-net-worth individuals across India.

More Featured Articles:

Startup India Registration: Unlocking Tax Benefits and Growth

ECB Rules Changed Big Time in 2026: What Indian Businesses Must Know to Unlock Global Funding.