Common Compliance Errors in GST, TDS & TCS Filings (FY 2026–27): Practical Insights, Legal Provisions & Expert Solutions.

A comprehensive guide on common GST, TDS, and TCS compliance errors for FY 2026–27. Learn key provisions, practical fixes, and expert strategies to avoid penalties, notices, and litigation risks.

📑 Common Compliance Errors in GST, TDS & TCS Filings – Practical Insights (FY 2026–27)

In the evolving landscape of Indian taxation, compliance under GST, TDS, and TCS has become increasingly data-driven and system-validated. With enhanced scrutiny, automated reconciliations, and AI-based risk profiling by authorities, even minor inconsistencies can trigger notices, penalties, or audits.

This detailed guide explores the most common compliance errors observed in FY 2026–27, along with legal provisions and practical solutions to mitigate risks and ensure robust compliance.

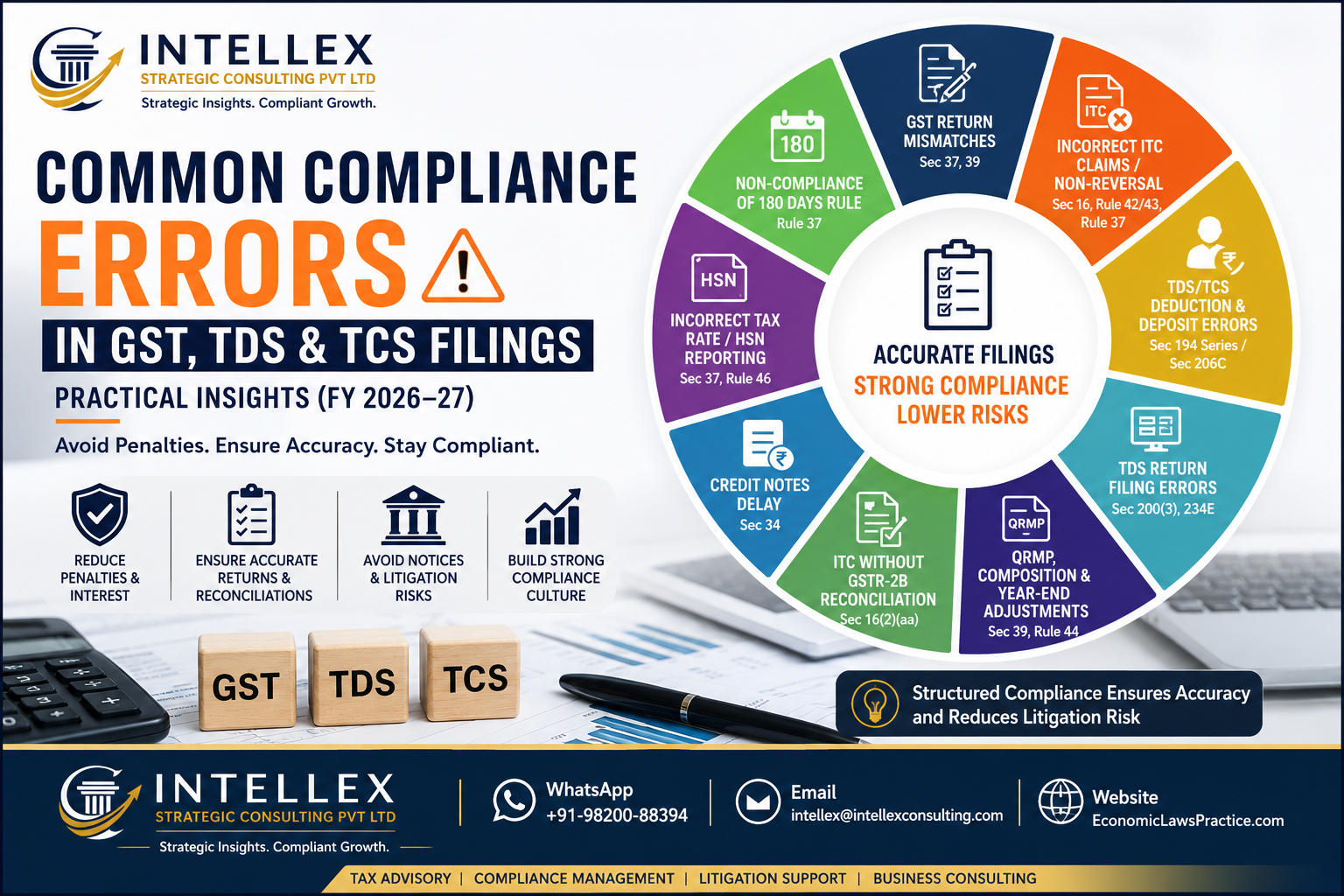

🔻 1. Mismatch in GST Returns (GSTR-1 vs GSTR-3B)

One of the most frequent triggers for departmental notices arises from discrepancies between outward supplies reported in GSTR-1 and tax liability discharged in GSTR-3B. Such mismatches often cascade into inaccuracies in annual returns (GSTR-9) and can attract interest liability.

Relevant Provisions: Section 37 & Section 39

Professional Insight:

A structured reconciliation between GSTR-1, GSTR-3B, and books of accounts is essential before filing. Leveraging GSTR-1A for corrections and implementing pre-filing validation checks can significantly reduce exposure.

🟧 2. Incorrect ITC Claim or Non-Reversal

Improper Input Tax Credit (ITC) claims continue to be a major area of litigation. Common lapses include claiming ineligible ITC, failing to reverse credit on exempt supplies, or ignoring the 180-day payment condition.

Relevant Provisions: Section 16, Rule 42/43, Rule 37

Professional Insight:

Businesses should adopt a strict reconciliation policy with GSTR-2B, ensure proper application of reversal rules, and actively monitor vendor payment cycles to avoid compliance gaps.

🟨 3. TDS/TCS Defaults – Deduction & Deposit Errors

Errors in deduction, delayed deposits, or incorrect application of rates under TDS and TCS provisions can lead to significant financial exposure.

Relevant Provisions: Section 194 Series / Section 206C

Professional Insight:

A robust compliance framework must include validation of applicable sections, adherence to deposit timelines (typically by the 7th of the following month), and periodic checks of rates and thresholds.

🔷 4. TDS Return Filing Errors (Forms 24Q / 26Q / 27Q)

Errors in TDS returns, especially PAN mismatches and incorrect challan mapping, often lead to defaults and correction filings.

Relevant Provisions: Section 200(3) & Section 234E

Professional Insight:

Pre-validation of PAN details, reconciliation with OLTAS, and timely correction filings through TRACES are essential to maintain clean compliance records.

🟪 5. QRMP, Composition & Year-End Adjustments Missed

Businesses under QRMP or composition schemes often overlook critical filings such as IFF, CMP-08, or GSTR-4, especially during year-end transitions.

Relevant Provisions: Section 39 & Rule 44

Professional Insight:

Periodic review of scheme-specific compliances and post-March reconciliations help ensure accuracy and prevent last-minute adjustments.

🔻 6. ITC Claimed Without GSTR-2B Reconciliation

Claiming ITC not reflected in GSTR-2B has become a high-risk area due to system-driven validations.

Relevant Provision: Section 16(2)(aa)

Professional Insight:

Adopting a strict 2B-based ITC policy, along with a vendor compliance tracking mechanism, is critical for sustainable compliance.

🟧 7. Delay in Reporting Credit Notes

Failure to report credit notes timely can distort tax liability and turnover reporting.

Relevant Provision: Section 34

Professional Insight:

Implementing a structured sales return tracking system and reconciling GSTR-1 with books ensures timely adjustments.

🟨 8. Incorrect Tax Rate or HSN Reporting

Misclassification of goods/services or incorrect tax rates can lead to short or excess tax payments and consequent notices.

Relevant Provision: Section 37 & Rule 46

Professional Insight:

Maintaining a standardized HSN master database and aligning it with e-invoicing data reduces classification risks.

🔷 9. Non-Compliance of 180 Days Rule

Failure to reverse ITC where vendor payments are not made within 180 days results in interest liability.

Relevant Provision: Rule 37

Professional Insight:

Vendor ageing reports and automated alerts should be integrated into accounting systems to ensure timely compliance.

🟪 10. Errors in Tax Liability Adjustment

Incorrect utilization of input credit or tax payments often leads to interest under Section 50.

Relevant Provisions: Section 39 & Section 50

Professional Insight:

Periodic reconciliation of liability registers and final validation before filing are crucial.

🔻 11. TCS Applicability Errors (Section 206C(1H))

Incorrect threshold calculations and misapplication of TCS provisions remain a common issue.

Relevant Provision: Section 206C(1H)

Professional Insight:

Accurate turnover tracking and customer-level reconciliation mechanisms are essential for compliance.

🟧 12. Late Filing of TDS Returns

Delayed filings attract a mandatory late fee of ₹200 per day and potential penalties.

Relevant Provisions: Section 234E & Section 271H

Professional Insight:

Maintaining a strict compliance calendar and internal deadlines ensures timely filings.

🟨 13. Non-Issuance of TDS Certificates

Failure to issue TDS certificates on time impacts both compliance and client relationships.

Relevant Provision: Section 272A(2)(g)

Professional Insight:

Automation of Form 16/16A generation and active monitoring of TRACES can eliminate delays.

🔷 14. ITC on Blocked Credits

Claiming ITC on ineligible expenses such as personal use or restricted categories leads to penalties and reversals.

Relevant Provision: Section 17(5)

Professional Insight:

Maintaining a blocked ITC checklist and improving expense classification systems is essential.

🟪 15. Filing Without Proper Final Review

A lack of structured review processes often results in avoidable errors being carried forward.

Relevant Provisions: Sections 16, 37, 39

Professional Insight:

Implementing a maker-checker system and a comprehensive pre-filing checklist significantly enhances compliance accuracy.

📊 Conclusion: The Case for Structured Compliance

In FY 2026–27, tax compliance is no longer a routine exercise but a strategic function requiring precision, automation, and continuous monitoring. Businesses that invest in structured compliance frameworks, reconciliation systems, and expert oversight are far better positioned to avoid litigation, reduce financial exposure, and maintain credibility with tax authorities.

🤝 Professional Support

For expert assistance in GST, TDS, and TCS compliance, reconciliations, audits, and advisory:

Intellex Strategic Consulting Pvt Ltd

📱 WhatsApp: +91-98200-88394

📧 Email: intellex@intellexconsulting.com

🌐 Website: EconomicLawsPractice.com

Specialists in taxation advisory, compliance management, and litigation support across India.

Intellex Strategic Consulting Pvt Ltd

More Featured Articles

Ultimate Guide to Singapore Company Registration 2026: Rules, Costs, and Compliance.

How Businesses in the UAE Can Stay Ahead of Compliance Demands in 2026.

Startup India Registration: Unlocking Tax Benefits and Growth

One thought on “Common Compliance Errors in GST, TDS & TCS Filings (FY 2026–27): Practical Insights, Legal Provisions & Expert Solutions.”