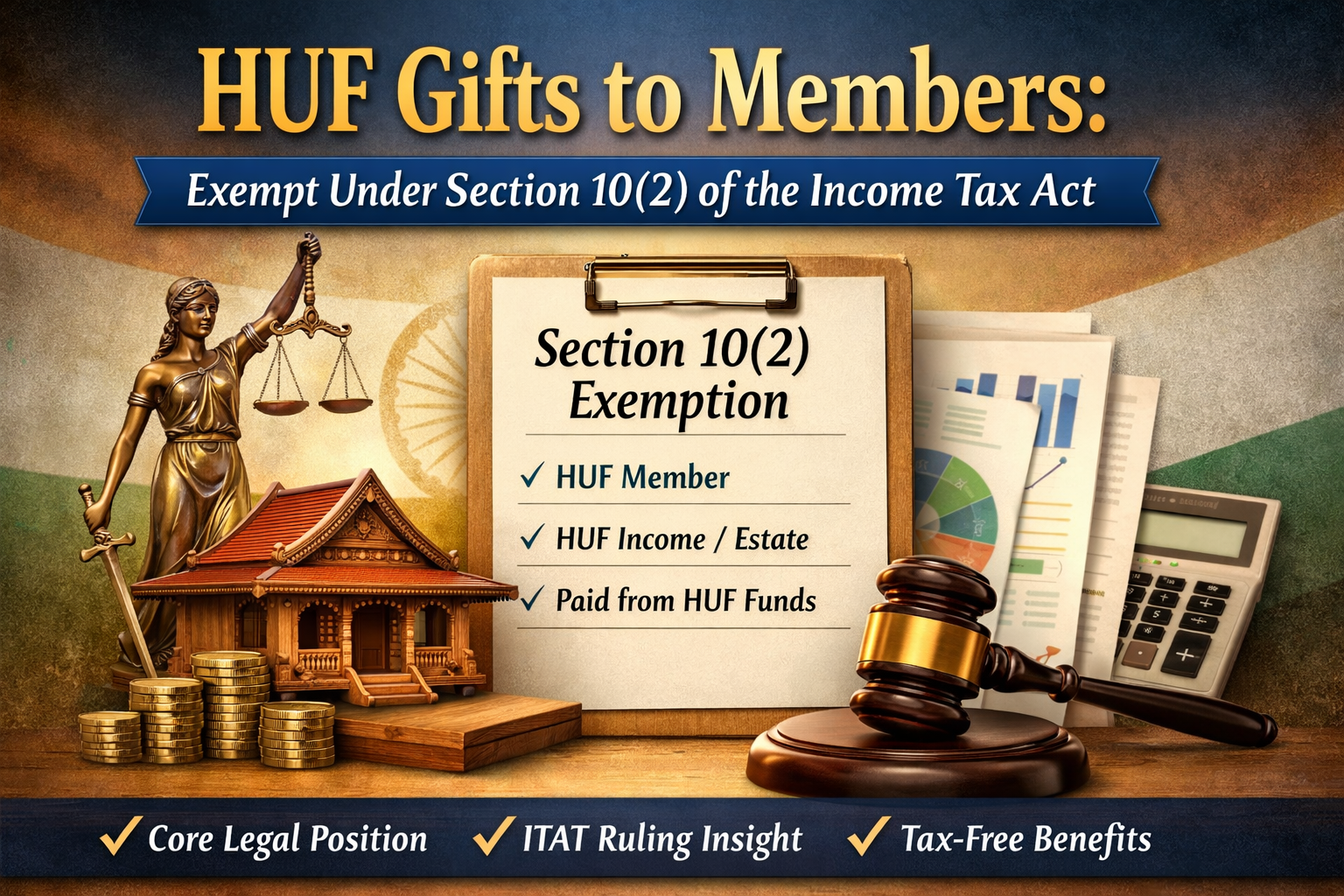

HUF Gifts to Members: Why They Are Exempt Under Section 10(2) of the Income Tax Act – A Legal & Practical Analysis.

Understand why gifts received by members from a Hindu Undivided Family (HUF) are exempt under Section 10(2) of the Income Tax Act. Learn legal provisions, ITAT rulings, and practical implications for taxpayers.

Introduction

The taxation of gifts received from a Hindu Undivided Family (HUF) continues to be an area of significant discussion and occasional misinterpretation. A recurring issue arises when tax authorities attempt to tax such receipts under Section 56(2)(vii) (now Section 56(2)(x)) of the Income Tax Act, 1961.

However, a careful reading of the law, supported by judicial precedents, clearly establishes that amounts received by a member from an HUF are exempt under Section 10(2), subject to certain conditions.

This article provides a detailed legal analysis, recent tribunal insights, and practical guidance for taxpayers and professionals.

Core Legal Position: Section 10(2) Explained

Section 10(2) of the Income Tax Act provides a specific exemption:

Any sum received by an individual as a member of a Hindu Undivided Family (HUF) is exempt, provided it is paid out of the income or estate of the HUF.

Three Essential Conditions for Exemption

To qualify for exemption under Section 10(2), the following conditions must be satisfied:

- Membership

The recipient must be a legitimate member of the HUF. - Existence of HUF Income or Estate

The HUF must have a valid income stream, corpus, or ancestral estate. - Source of Payment

The amount received must be paid out of such income or estate.

When these conditions are fulfilled, the exemption is automatic and unconditional.

The Misinterpretation Around Section 56(2)(vii)

A common misunderstanding arises due to the provisions of Section 56(2)(vii) (now replaced by Section 56(2)(x)), which taxes gifts received without consideration unless they fall within specified exceptions.

Where the Confusion Begins

The Explanation to Section 56 includes the definition of “relative,” which states:

- In case of an HUF, any member thereof is considered a relative.

This leads to confusion regarding whether:

- An HUF can be treated as a “relative” when it gives a gift to a member.

Correct Legal Interpretation

- The definition applies only when the HUF is the recipient (donee).

- It clarifies that a member giving to HUF is treated as a relative.

- It does NOT address situations where the HUF is the donor.

Therefore:

Section 56(2)(vii) does not override Section 10(2), which specifically governs HUF-to-member distributions.

Judicial Perspective: ITAT Ruling in Seema Sureka Case

A recent and significant development comes from the ITAT ruling in:

Seema Sureka vs ACIT (ITA No. 2682/Kol/2024)

Key Observations by ITAT

- Conflicting Tribunal Views Exist

- Different ITAT benches have taken varying positions on whether an HUF qualifies as a “relative.”

- However, no High Court or Supreme Court ruling exists against the assessee’s position.

- Preference for Logical Interpretation

- The Tribunal relied on the reasoning in Gyanchand M. Bardia (Jaipur ITAT).

- It clarified that:

- The term “relative” in Section 56 refers to the relationship of the donor to the donee.

- In HUF-to-member transactions, Section 10(2) is the appropriate provision.

- Matter Remanded for Verification

- The ITAT did not confirm taxability.

- Instead, it directed the Assessing Officer (AO) to:

- Verify HUF membership

- Examine existence of corpus/income

- Confirm that payment was from HUF funds

Key Takeaways from the Ruling

- The ITAT did not endorse taxation under Section 56.

- It reinforced that:

- Section 10(2) is the governing provision

- Exemption applies if factual conditions are met

- The burden is primarily on documentation and substantiation, not legal interpretation.

Practical Implications for Taxpayers

1. Strong Documentation is Critical

Maintain proper records such as:

- HUF deed

- Capital account statements

- Bank statements reflecting payments

- Evidence of HUF income or corpus

2. Avoid Misclassification

Ensure that:

- Payments are clearly recorded as distribution from HUF

- Not treated as individual gifts

3. Be Prepared for Scrutiny

While the legal position is favorable, tax authorities may:

- Question the nature of the transaction

- Seek evidence of genuineness

4. Professional Structuring Matters

Improper structuring may lead to:

- Unnecessary litigation

- Tax additions under Section 56

Conclusion

The legal framework is clear and taxpayer-friendly:

Gifts or distributions from an HUF to its members fall squarely within the exemption provided under Section 10(2), provided the prescribed conditions are satisfied.

The recent ITAT ruling in Seema Sureka strengthens this position by emphasizing that:

- Section 56(2)(vii) cannot override a specific exemption provision

- The focus should be on factual verification, not legal ambiguity

With proper planning, documentation, and compliance, HUF-to-member distributions can remain fully tax-exempt, offering an effective tool for family wealth management.

How We Can Help

Intellex Strategic Consulting Private Limited specializes in:

- HUF structuring and tax optimization

- Income tax advisory and litigation support

- Compliance and documentation strategies

📞 WhatsApp / Mobile: +91-98200-88394

📧 Email: intellex@intellexconsulting.com

🌐 Web: www.intellexconsulting.com | www.intellexcfo.com

Team – Intellex Strategic Consulting Pvt Ltd

More Featured Posts:

New Income-tax Act 2025: Key Features, Major Changes & What It Means for Taxpayers in India.

How Ex-Bankers Can Build a High-Income Second Career Through a Corporate DSA Partner Program

Why MSMEs Trust Us With Their Most Critical Financial Decisions

Loans Takeover proposals with enhancement of Banking limits for MSME Sector Companies

Startup India Registration: Unlocking Tax Benefits and Growth

Ultimate Guide to Singapore Company Registration 2026: Rules, Costs, and Compliance.

3 thoughts on “HUF Gifts to Members: Why They Are Exempt Under Section 10(2) of the Income Tax Act – A Legal & Practical Analysis.”