Lump-Sum Alimony vs Monthly Maintenance: Tax Treatment Under Indian Income Tax Law – A Complete Guide

Understand the tax implications of lump-sum alimony vs monthly maintenance in India. Learn what is taxable, key court rulings, and smart tax planning strategies for matrimonial settlements.

Introduction

The tax treatment of alimony and maintenance payments in India remains a complex and evolving area due to the absence of explicit provisions under the Income-tax Act, 1961. This ambiguity often leads to disputes between taxpayers and the Revenue authorities, especially regarding whether such receipts should be treated as taxable income or non-taxable capital receipts.

Understanding the distinction between lump-sum alimony and monthly maintenance is crucial for individuals undergoing matrimonial settlements, divorce proceedings, or financial restructuring post-separation.

Absence of Specific Legal Provision

The Income-tax Act does not explicitly define or govern the taxability of matrimonial settlements. As a result:

- Tax authorities often invoke Section 56(2) (Income from Other Sources)

- In some cases, capital gains provisions are examined

However, due to the personal nature of such payments, courts have consistently relied on fundamental tax principles rather than strict statutory interpretation.

Core Tax Principles Applied by Courts

Indian courts have applied two key principles:

1. Capital vs Revenue Receipt

- Capital receipts → Generally not taxable

- Revenue receipts → Generally taxable

2. Source and Regularity of Income

For any receipt to qualify as income:

- It must arise from a definite source

- It should have recurrence or periodicity

These principles form the backbone of judicial interpretation in matrimonial tax cases.

Landmark Judicial Precedent

A critical ruling in this domain is:

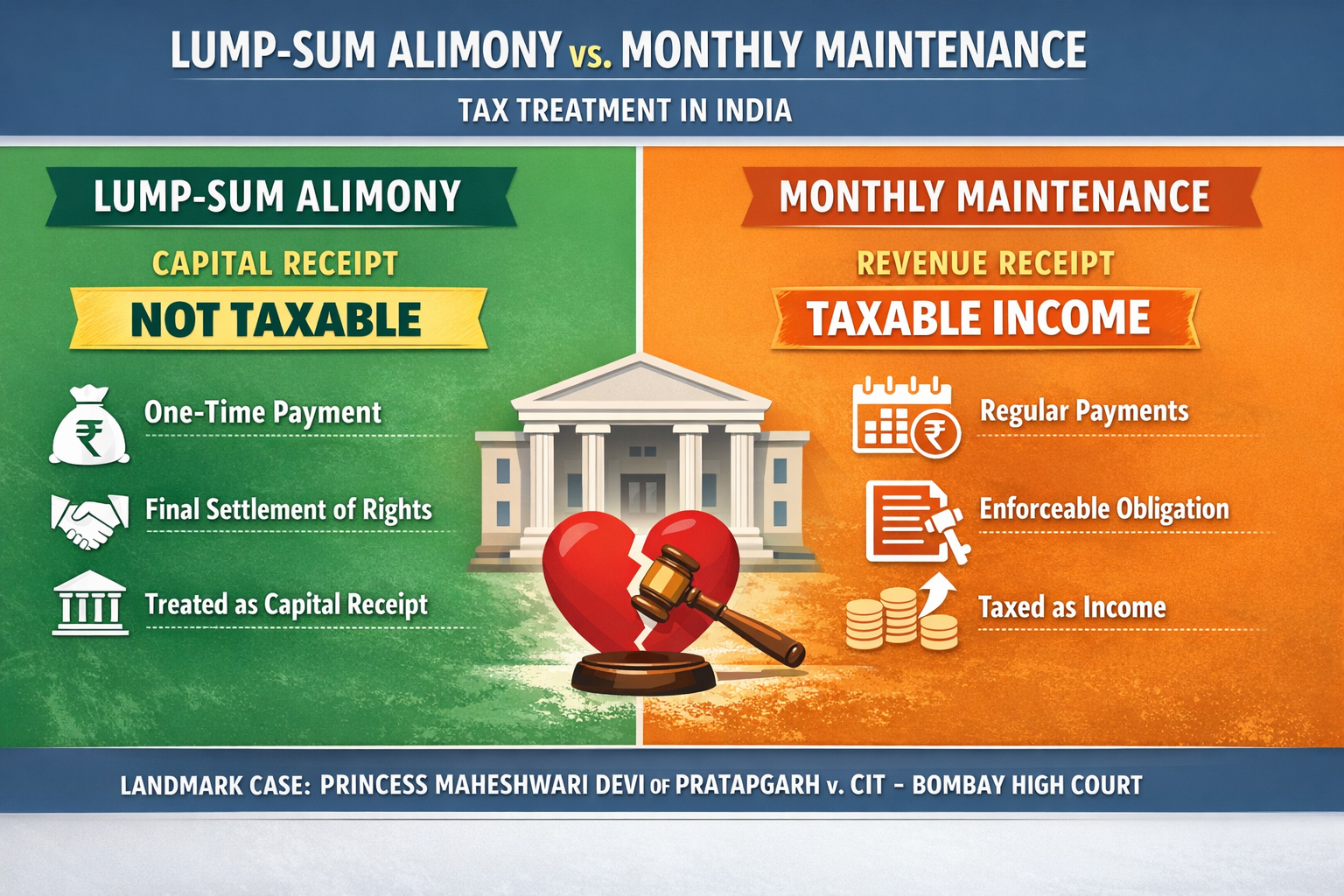

Princess Maheshwari Devi of Pratapgarh v. CIT

The Bombay High Court held that:

- Periodic maintenance payments are taxable

- Reason: They are recurring, arise from a legal obligation, and therefore qualify as income

This judgment continues to serve as a guiding precedent in similar cases.

Tax Treatment of Lump-Sum Alimony

Nature

- One-time settlement

- Paid in full and final discharge of marital rights

Tax Position

- Considered a capital receipt

- Not taxable under Indian tax law

Judicial Reasoning

- It represents a settlement of personal rights

- It lacks periodicity or recurring nature

- It is not derived from a regular income source

Practical Insight

Lump-sum alimony is often preferred for:

- Tax efficiency

- Financial closure

- Avoiding future litigation

Tax Treatment of Monthly Maintenance

Nature

- Paid periodically (monthly/quarterly)

- Based on ongoing obligation

Tax Position

- Treated as income

- Taxable under “Income from Other Sources”

Reasoning

- Recurring in nature

- Arises from enforceable legal right

- Comparable to a regular income stream

Property Transfers in Divorce Settlements

This is one of the most complex areas in matrimonial taxation.

Legal Framework

Under Section 47, certain transfers are not regarded as transfer for capital gains purposes. However:

- Divorce-related transfers are not explicitly covered

Judicial Interpretation

Courts have generally held:

- Such transfers are not commercial transactions

- They are adjustments of mutual rights

- Hence, may not attract capital gains tax in many cases

Key Consideration

Each case depends on:

- Nature of settlement

- Documentation

- Intent behind transfer

Emerging Judicial Consensus

Based on multiple rulings, the legal position is now relatively settled:

✔ Lump-Sum Alimony

- Capital receipt

- Not taxable

✔ Periodic Maintenance

- Revenue receipt

- Taxable as income

Strategic Tax Planning Insights

For individuals and advisors:

Choose Lump-Sum When Possible

- Offers tax advantage

- Eliminates recurring tax liability

Structure Agreements Carefully

- Clearly define nature of payment

- Avoid ambiguity between “maintenance” and “settlement”

Document Intent

- Agreements should explicitly state:

- Full and final settlement

- No future claims

Evaluate Property Transfers

- Seek professional advice to:

- Avoid unintended capital gains exposure

- Ensure compliance

Common Mistakes to Avoid

- Treating all alimony as tax-free

- Poorly drafted settlement agreements

- Ignoring tax implications of property transfers

- Not reporting taxable maintenance income

Conclusion

The taxation of alimony in India is driven more by judicial interpretation than statutory clarity. The distinction between lump-sum (capital) and periodic (revenue) payments is crucial and can significantly impact tax liability.

With increasing scrutiny by tax authorities, it is essential to structure matrimonial settlements strategically and compliantly.

Team : Intellex Strategic Consulting Pvt Ltd

More Featured Articles:

New Income-tax Act 2025: Key Features, Major Changes & What It Means for Taxpayers in India.

Tax Loss Harvesting: A Strategic Guide to Reducing Capital Gains Tax.

Secured and Un-Secured Financial Products from Bajaj Finance Ltd

Startup India Registration: Unlocking Tax Benefits and Growth

2 thoughts on “Lump-Sum Alimony vs Monthly Maintenance: Tax Treatment Under Indian Income Tax Law – A Complete Guide.”