Search and Seizure under the Income-tax Act, 2025: Complete Guide to Tax Raids, Digital Investigations, Asset Seizure and Block Assessment in India.

Comprehensive guide to Search and Seizure provisions under the Income-tax Act, 2025 effective from 1 April 2026. Learn about tax raids, digital searches, powers of tax authorities, taxpayer rights, block assessment, asset seizure, and compliance strategies for businesses and individuals.

Search and Seizure under the Income-tax Act, 2025: A Comprehensive Analysis.

The Government of India has introduced the new Income-tax Act, 2025, which will come into force from 1 April 2026. Among the most significant enforcement provisions under the new legislation are the Search and Seizure provisions contained in Sections 247 to 259.

These provisions replace the corresponding provisions under the Income-tax Act, 1961, including Sections 132, 132A and related provisions that historically governed income tax raids, seizure of assets, requisition of documents, and investigation of undisclosed income.

The new framework reflects the evolving nature of financial transactions, increasing digitization of business operations, and the growing importance of electronic evidence in tax investigations. The legislation grants extensive powers to tax authorities while simultaneously preserving procedural safeguards intended to protect taxpayers from arbitrary action.

This article provides a detailed examination of the Search and Seizure framework under the Income-tax Act, 2025, its implications for taxpayers, and the compliance measures businesses should adopt.

Legislative Objective Behind Search and Seizure Provisions

Search and seizure provisions are among the strongest enforcement mechanisms available to tax authorities. Their primary objective is to:

- Detect tax evasion.

- Identify undisclosed income and assets.

- Gather evidence of financial irregularities.

- Prevent destruction or concealment of records.

- Protect government revenue.

The legislature recognizes that ordinary assessment proceedings may not always be sufficient where taxpayers deliberately conceal income or maintain unaccounted assets. Search operations therefore serve as investigative tools to uncover hidden financial information.

Section 247 – Search and Seizure

Section 247 serves as the cornerstone of the search and seizure framework and broadly corresponds to the erstwhile Section 132 of the Income-tax Act, 1961.

A search may be authorized when the competent authority possesses credible information and has reason to believe that a person:

1. Has Failed to Produce Documents

Despite being served with summons or notices, the person has failed to produce books of account, records, or other relevant information.

2. Is Likely to Withhold Information

Even if no default has yet occurred, authorities may act where there is a reasonable belief that the taxpayer is unlikely to produce records when called upon.

3. Possesses Undisclosed Income or Assets

Authorities may authorize a search where information suggests the existence of:

- Undisclosed income

- Unaccounted cash

- Hidden investments

- Benami assets

- Unreported business transactions

- Undisclosed foreign assets

- Other concealed property

The existence of “reason to believe” remains a crucial legal safeguard and cannot be replaced by mere suspicion or conjecture.

Powers of the Authorised Officer During a Search

Once a valid warrant of authorization has been issued, the authorized officer receives extensive statutory powers.

These include the power to:

Enter and Search Premises

The officer may enter and inspect:

- Residential premises

- Business establishments

- Warehouses

- Factories

- Shops

- Offices

- Vehicles

- Aircraft

- Vessels

where relevant information or assets are believed to be located.

Inspection of Books and Records

Authorities may inspect:

- Physical books of account

- Financial records

- Contracts

- Invoices

- Agreements

- Ledgers

- Audit documents

for evidentiary purposes.

Search of Individuals

Where circumstances warrant, individuals present at the premises may be searched if there is reason to believe that books, documents, money, jewellery or other valuable articles are concealed on their person.

Preparation of Inventory

Detailed inventories are prepared covering:

- Cash

- Jewellery

- Bullion

- Precious stones

- Valuable articles

- Documents

- Stock records

Such inventories become important evidence in subsequent proceedings.

Digital Search Powers: A Major Feature of the Income-tax Act, 2025

One of the most notable developments in the new law is its explicit recognition of digital assets and electronic evidence.

Modern businesses increasingly maintain records electronically rather than in physical form. Consequently, the Act expands search powers to cover digital ecosystems.

Authorities may now access:

- Computer systems

- Laptops

- Servers

- Mobile devices

- Cloud storage accounts

- Digital databases

- Email communications

- Electronic records

- Accounting software

- Enterprise resource planning (ERP) systems

Access Codes and Technical Assistance

The authorized officer may require:

- Passwords

- Encryption keys

- Authentication credentials

- Access codes

- Technical support

to facilitate examination of digital records.

Failure to cooperate may result in legal consequences.

This digital expansion significantly enhances the ability of tax authorities to investigate sophisticated financial arrangements and hidden transactions.

Power to Break Open Locks and Override Access Restrictions

The law empowers authorized officers to:

- Break open locks where access is denied.

- Override electronic access restrictions.

- Access digital repositories.

- Secure evidence that may otherwise be destroyed or concealed.

Such powers may be exercised only during a validly authorized search operation.

Seizure of Books, Documents and Assets

During a search operation, authorities may seize:

- Books of account

- Financial records

- Digital devices

- Electronic storage media

- Cash

- Jewellery

- Bullion

- Valuable articles

However, stock-in-trade generally cannot be seized. Instead, inventory records are prepared and documented.

This distinction is intended to avoid unnecessary disruption of business operations.

Requisition of Assets and Documents

The new Act continues provisions corresponding to the earlier Section 132A.

Where books, documents or assets are already in the custody of another authority, tax authorities may requisition such materials.

Examples include records held by:

- Customs authorities

- Enforcement agencies

- Police departments

- Regulatory authorities

- Other government agencies

This enables inter-agency cooperation in combating tax evasion and financial misconduct.

Application of Seized Assets

The provisions corresponding to former Section 132B govern the treatment of seized assets.

Seized assets may be adjusted against:

- Outstanding tax liabilities

- Interest liabilities

- Penalties

- Other amounts legally recoverable under tax laws

Any surplus remaining after adjustment must be returned to the taxpayer in accordance with prescribed procedures.

Procedural Safeguards Available to Taxpayers

Although search and seizure powers are extensive, the law incorporates important safeguards.

Requirement of “Reason to Believe”

The competent authority must possess credible information leading to a bona fide belief that conditions for search exist.

Searches cannot be initiated merely on:

- Rumours

- Suspicion

- Anonymous allegations without verification

Valid Warrant of Authorization

Every search must be supported by a legally valid authorization.

Absence of proper authorization may render proceedings vulnerable to judicial challenge.

Independent Witnesses

Search proceedings are generally conducted in the presence of independent witnesses.

This helps ensure transparency and credibility.

Panchnama

A Panchnama records:

- Time of commencement and conclusion

- Assets found

- Documents seized

- Statements recorded

- Inventory details

The Panchnama often becomes critical evidence in litigation.

Judicial Review

Courts retain the power to review:

- Legality of authorization

- Abuse of power

- Procedural violations

- Constitutional violations

Taxpayers continue to enjoy legal remedies against arbitrary or unlawful searches.

Rights and Responsibilities of Taxpayers During a Search

Taxpayers should:

- Cooperate with authorized officers.

- Provide access to records.

- Maintain transparency.

- Seek copies of inventories and Panchnama.

- Record concerns where procedural irregularities occur.

At the same time, taxpayers retain rights to:

- Professional representation.

- Fair treatment.

- Protection against unlawful action.

- Judicial remedies.

Proper legal guidance during a search operation can significantly affect subsequent proceedings.

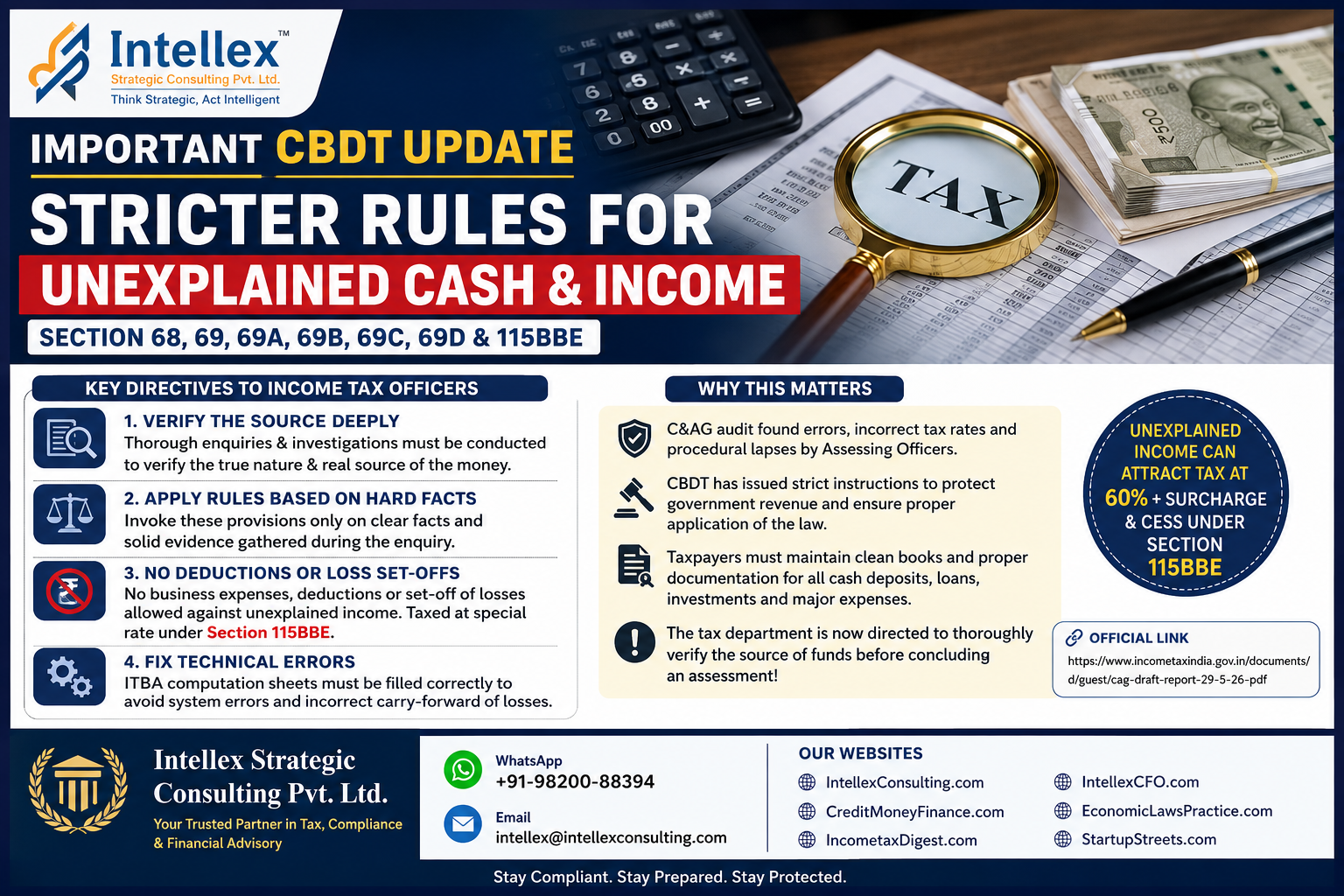

Block Assessment – The New Framework for Undisclosed Income

One of the most important consequences of a search operation is Block Assessment.

Block Assessment is a special assessment mechanism used to determine undisclosed income detected during a search.

Applicability

The revised framework applies to searches conducted on or after 1 September 2024.

Objective

Instead of conducting separate assessments for multiple years, authorities consolidate undisclosed income discovered during the search into a single block assessment proceeding.

This enables faster and more efficient tax administration.

Tax Rate

Undisclosed income assessed under the block assessment regime is generally subject to a flat tax rate of 60%.

This significantly increases the financial consequences of maintaining unaccounted income or assets.

Scope of Income Covered

Block assessment may cover:

- Unrecorded business income

- Unexplained cash

- Unaccounted investments

- Undisclosed foreign assets

- Bogus transactions

- Suppressed turnover

- Unexplained expenditure

The block assessment process has become a central enforcement mechanism in India’s anti-tax-evasion framework.

Impact on Businesses and High-Net-Worth Individuals

The enhanced search powers under the Income-tax Act, 2025 signal the government’s continued focus on:

- Tax transparency

- Digital investigations

- Data-driven enforcement

- Financial accountability

Businesses should proactively strengthen:

- Accounting systems

- Internal controls

- Digital record management

- Compliance monitoring

- Tax documentation practices

High-net-worth individuals and family offices should also undertake periodic compliance reviews to identify potential risks before they attract regulatory scrutiny.

Best Practices for Tax Compliance

Organizations should consider:

Regular Tax Health Checks

Periodic review of tax positions and documentation.

Digital Record Management

Maintaining organized and accessible digital records.

Internal Compliance Audits

Identifying gaps before regulatory intervention.

Proper Documentation

Supporting transactions with adequate evidence.

Professional Advisory Support

Obtaining expert guidance on tax investigations, assessments, and litigation.

How Intellex Strategic Consulting Pvt. Ltd. Can Help

Search and seizure proceedings can have significant financial, operational and reputational consequences. Professional assistance is critical in managing investigations, responding to notices, preparing representations and handling block assessments.

Our Services

Intellex Strategic Consulting Pvt. Ltd. provides comprehensive advisory and compliance support relating to:

- Income Tax Search and Seizure Matters

- Block Assessment Proceedings

- Tax Investigation Support

- Tax Litigation Assistance

- Corporate Tax Compliance

- Regulatory Advisory

- Financial Due Diligence

- Digital Documentation Review

- Risk Assessment and Compliance Audits

Contact Details

Intellex Strategic Consulting Pvt. Ltd.

WhatsApp: +91-98200-88394

Email: intellex@intellexconsulting.com

Websites:

- IntellexConsulting.com

- CreditMoneyFinance.com

- IncometaxDigest.com

- IntellexCFO.com

- EconomicLawsPractice.com

- StartupStreets.com

Conclusion

The Search and Seizure provisions under the Income-tax Act, 2025 represent a modernized and technologically advanced enforcement framework designed to tackle tax evasion in an increasingly digital economy. While the law grants extensive investigative powers to tax authorities, it also preserves critical procedural safeguards such as the requirement of “reason to believe,” valid authorization, independent witnesses, and judicial oversight.

With enhanced digital search capabilities, cloud access provisions, and a stringent block assessment regime imposing a flat 60% tax on undisclosed income, taxpayers must adopt a proactive compliance approach. Businesses, professionals, family offices, and high-net-worth individuals should ensure robust documentation, transparent financial reporting, and regular compliance reviews to minimize risks and effectively navigate the evolving tax enforcement landscape in India.

EconomicLawsPractice.com

More Featured Articles:

Startup India Registration: Unlocking Tax Benefits and Growth